This is the fourth in a series of columns that will look at real estate issues in Sweetwater County. What you need to know before you buy a house. What information you could use prior to renting an apartment. How you can maintain and enhance your existing housing.

One of the key elements in securing a mortgage for a house or being able to rent an apartment is your credit history. In most cases, your credit history is being tracked through three major national credit reporting bureaus. The credit reports that they maintain on you help your bank decide whether they will approve a mortgage for you to buy that cute ranch house in Green River. Those credit reports on you also help your potential landlord in Rock Springs decide whether they will approve a lease for you to move into that two-bedroom unit with the kitchen you fell in love with during your recent visit.

Making sure that those credit reports include accurate information is critical to you getting a new home. The information in your credit reports is used to create credit scores. Those credit scores are utilized by a variety of businesses and organizations that lend money to people like you.

An accurate credit report can help you. A credit report that includes incomplete or inaccurate information can hurt you.

Even if you’re approved for a mortgage, for example, the accuracy of your credit reports can hurt you in ways not so obvious in the beginning. Your mortgage rate may be higher if your credit report does not reflect your true credit history. Over time, you may pay substantially more in interest payments than someone else whose credit report indicates that they are a better credit risk as seen by the lender.

As noted in a previous installment, residents of Sweetwater County as well as people throughout the United States are able to get three free credit reports annually from the major national credit reporting firms: Equifax, Experian, and TransUnion.

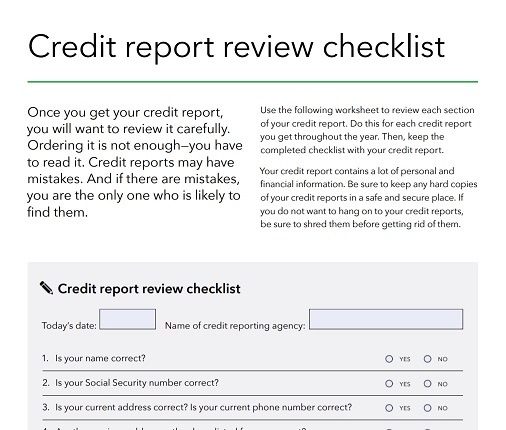

Getting a copy of one of your credit reports is just the beginning. You need to review it to make sure that the information included is accurate and complete.

Among the items you’ll want to check for accuracy and completeness are:

Personal Information: Name, Address, Social Security Number, Employer

Credit Information: Bank accounts, Credit accounts, Loans, Credit limits, Account balances, Payment history

Public Records: Collection agency activities, Bankruptcies, Foreclosures, Lawsuits

Inquiries: Businesses and organizations that have reviewed your credit report

You can view a checklist to follow by clicking HERE. (This Credit Report Review Checklist was prepared by Consumer Financial Protection Bureau.)

You’re likely the only one to know for sure what items are missing or what information is not necessarily accurate. You have the right, according to the Federal Trade Commission (FTC), to correct errors, have certain information removed, and have certain information added to your credit reports.

“Both the credit reporting company and the information provider (that is, the person, company, or organization that provides information about you to a consumer [credit] reporting company) are responsible for correcting inaccurate or incomplete information in your [credit] report,” according to the FTC. “To take full advantage of your rights under this law, contact the credit reporting company and the information provider.”

Image was provided courtesy of the Consumer Financial Protection Bureau.

If you find something wrong or missing from your credit report, you would typically first contact the credit reporting entity that issued the credit report to you – Equifax, Experian, or TransUnion. The FTC reports that those credit bureaus “must investigate the items in question — usually within 30 days — unless they consider your dispute frivolous. They also must forward all the relevant data you provide about the inaccuracy to the organization that provided the information.

After the information provider receives notice of a dispute from the credit reporting company, it must investigate, review the relevant information, and report the results back to the credit reporting company. If the information provider finds the disputed information is inaccurate, it must notify all three nationwide credit reporting companies so they can correct the information in your file.”

After both the credit reporting entity and the source of the information finish their investigation, the FTC states that “the credit reporting company must give you the written results and a free copy of your report if the dispute results in a change. (This free report does not count as your annual free report.) If an item is changed or deleted, the credit reporting company cannot put the disputed information back in your file unless the information provider verifies that it is accurate and complete. The credit reporting company also must send you written notice that includes the name, address, and phone number of the information provider.”

The FTC recommends that you also contact the information provider directly “in writing that you dispute an item. Many providers specify an address for disputes. If the provider reports the item to a credit reporting company, it must include a notice of your dispute. And if you are correct — that is, if the information is found to be inaccurate — the information provider may not report it again.”

What happens if the investigation doesn’t resolve the dispute to your liking?

“…You can ask that a statement of the dispute be included in your file and in future reports,” states the FTC. “You also can ask the credit reporting company to provide your statement to anyone who received a copy of your [credit] report in the recent past. You can expect to pay a fee for this service.”

In addition, the FTC indicates that “if you tell the information provider that you dispute an item, a notice of your dispute must be included any time the information provider reports the item to a credit reporting company.”

The Federal government has issued a document detailing your rights in this matter, A Summary of Your Rights Under the Fair Credit Reporting Act. You can view this document by clicking HERE.

In future news columns, we’ll detail how you can create a credit history if you don’t have one, how you can enhance your current credit situation, and what steps you’ll need to take if you’ve lost or had a credit card stolen as well as if you’re a victim of identity theft. We’ll also explain how all of these aspects of your credit history tie together in the form of your credit scores.

Your credit history is critical if you’re going to buy or rent a home in Sweetwater County.

Do you have ideas for future Real Estate columns?

Your questions may be used in a future news column.

Contact Richard McDonough at [email protected].

© 2020 Richard McDonough